Let’s have some fun and talk about apartment building APODs! You know, Annual Property Operating Data statements. I know, you’re wondering how will that be fun? Just wait! You’ll learn how listing agents use these figures all the time to create wonderful-looking GRMS[1] and cap. rates[2]. By magic and slight-of-hand, apartment expenses become 25% of gross operating income! Reserves and management fees disappear. Actual rent is replaced by proforma rent. Is proforma even a real word?

Let’s have some fun and talk about apartment building APODs! You know, Annual Property Operating Data statements. I know, you’re wondering how will that be fun? Just wait! You’ll learn how listing agents use these figures all the time to create wonderful-looking GRMS[1] and cap. rates[2]. By magic and slight-of-hand, apartment expenses become 25% of gross operating income! Reserves and management fees disappear. Actual rent is replaced by proforma rent. Is proforma even a real word?

Now why would someone do this? Do you remember your senior prom? You spent hours picking out what you would wear – yes, men too. If you didn’t own something quite right you’d go out and buy or rent it! A clip-on was OK, or so I was told. You wanted to look your best because this was a special event, right?

A sale is a special event. You only get one chance to make a great first impression. OK, no more banal clichés. So, as the listing agent, you want to have the flyer, video, spreadsheet, background data and demographic overview present the property in the best possible light. On the numbers side you want the GRM as low as possible and the cap. rate as high as possible. And you need to do this without losing all credibility – quite the balancing act! This is where the magic comes in!

To get a true picture of the financial status of the apartment building under consideration, smart buyers and selling agents will look past the listing agent’s glamorous presentation and drill down to the true picture of income and expenses. To do this, you need to have brokered hundreds of sales and reviewed hundreds of these statements like I have or read this handy-dandy cheat sheet!

Working magic with income figures

Now, there aren’t many things you can do with the current rents. They are what they are right? Well, even light waves can bend. I’ve seen the APOD only reflect proforma rents with notations that the units are “currently rented to family members” or “month to month tenancies” or other dismissive language that says, “Don’t look here; move on!” I’ve seen current rents mentioned, but the analysis only comprehends proforma rents. OK; I’ve done this.

What about proforma rents? Has the listing agent included a rent survey? Probably not. Usually, the proforma rents just appear in a column without any backup data. Doing a rent survey is drudge work and, like my fellow brokers, I hate doing it. However, it is the most accurate way to estimate proforma rents if the survey is unbiased. Good luck getting an unbiased rent survey in a listing agent’s package. Do you want a true picture of proforma rents? Just do the drudge work yourself or have your broker do it.

A local alternative would be to use the summary chart for the subject’s sub-area in the Dyer Sheehan Apartment Market Survey[3]. Sometimes I’ll use this but doing an actual rent survey yourself is best.

What about vacancy factor / credit losses? In the real world these always exist. There is always down time between tenancies and collection issues are common. Does this line item reflect the real-world market? Think about it – if your average turnover is say 10 days of turnover work every two years you have an inherent 1.4% vacancy factor even if you rented the apartment on day one. If it took you say seven days to rent the unit on top of the turnover period, you have a 2.3% vacancy factor.

If the GOI[4] in the seller’s books does not reflect the listing agent’s APOD figures, ask why. Is the vacancy factor / collection loss factor higher? Were there some evictions? Is there excessive turnover or downtime? Why?

Working magic with expense figures

Now let’s get to the real problem area in apartment building APODs – expense line items. Here’s where creativity, inexperience, stupidity and little white lies go head to head!

I’ll go in the order of the CCIM APOD[5]. Sorry, another acronym – CCIM – Certified Commercial Investment Member. This is a very prestigious, hard to obtain commercial real estate designation. A CCIM designation involves a serious investment of time and money and, in my opinion, is the highest and most respected professional designation a commercial real estate broker can obtain. If your real estate agent is a CCIM you’re typically in very good hands! My hands are good too though and I have other acronyms after my name and four decades of experience.

Other Income

This would be income from laundry machines, vending machines, parking, etc. Sometimes a broker will “estimate” this as the books may be mysteriously unavailable when the APOD preparation deadline is imminent or the income is “off-books” as in unreported cash income.

Real Estate Taxes

This is another one of my favorites! Listing agents will commonly project 1% of the list price here. That’s it right? Well, look at the current actual tax bill – available online in Santa Barbara county. You’ll find a smorgasbord of additional fees and charges: vector management, flood control, improvement district fees, sewer fees, school bonds, park bonds, library bonds, James Bonds etc. Ever-inventive government loves to tack on additional items to the real estate tax bill to fund an expansive and rather impressive array of dozens of things that never seem to go away. Do you wonder why a sewer charge that is based on water volume is on your tax bill or why there is a new school bond every few years? Sorry; there are no good answers here; just be aware of the additional charges.

I break out the real estate taxes into two lines: the basic 1% charge based on the list price or analysis price and then everything else from the latest tax bill. Now some of these things will change, but I don’t want to research each agency and their formulas. I have a life you know!

Property Insurance

Many people underinsure their properties intentionally or not. Insurance brokers will often quote building and contractor prices from statistical resources that lump Los Angeles and Santa Barbara together. You’ll know from our gas prices and experiences with many local contractors that we are considered a “cornered market”. That means, due to lack of competition, you pay more. Sorry, not sorry. So, an expected bid of $150 PSF for construction costs jumps over the moon here, even for your modest Isla Vista mansion.

The solution: Get a new insurance quote with real Santa Barbara area building costs or that offers guaranteed replacement. As a buyer, this is what you will be paying unless your insurance broker continues to underestimate local construction costs. Do I do this? Not usually. I tend to use whatever the seller provides unless it seems absurdly high or low. What me worry?

Off site and on-site management

If the seller is paying 6% for off-site management, why is the listing broker using 4%? It makes the bottom line look better that’s why! If you own 200 units your fee will be less. If this smaller building is your only managed property you’re gonna pay retail!

My favorite egregious line-item fudge is to have the listing broker not include any off-site management and include payments to an on-site “manager” as a slight rent discount. This is common, but silly since, in most cases, it would be a violation of law. There are specific formulas to recompense a resident manager spelled out in California real estate law including apartment discounts. Learn what they are and use them.

Payroll

What? Yes; in larger complexes you may have several employees involved in site operations and they get paid! I’m talking about people who only work for you regularly. And yes, your resident manager and other employees need workers’ comp. insurance, withholding and all the other items required for any employee. Don’t think any of your worker bees are “independent contractors”. If they only regularly work for the complex they are employees and subject to all the wonderful benefits and red tape of employee management. This would include the next two lines items – Expenses/Benefits and Taxes/Workers’ Compensation. (Yes, the apostrophe is in the right place). Sometimes, these employees and related expenses disappear on an APOD. Maybe they’re on vacation?

Repairs and Maintenance

This is a prime line-item ripe for abuse. The listing agent should just use actual maintenance expenses, right? I do this on occasion, but it can be very misleading. Does the total represent a 12-month extrapolation of the past three months, past 12 months, the past calendar year, an average of the past three to five years or what? Being “selective” in the base period used may produce vastly different figures. Maybe there’s an ongoing slab leak issue that occurred in March. Ouch! Well, if we start the 12-month period in April, problem solved!

I’ve seen this line item expressed as a percentage of GOI. I’ve also seen it as a price per unit allocation. I use the latter method. I don’t want to audit the maintenance expenditures to break out capitalized items. I could get carpel tunnel! I consult with Apartment Building Appraisers & Analysts, Inc. annual workbook for Southern California[6] to get a realistic estimate. This is a wonderful resource for obtaining apartment building expense guidelines.

Utilities

These are “hard costs” and are hard for your listing agent to fudge. See how I did that! However, it can be done! I’ve seen electricity and gas expenses set at zero when I know there are separate house meters for these utilities for outside lights, laundry machines and “clean and show” costs.

Refuse is another shaky one. Is this line item just for refuse only or does it include the often-substantial charges for extra pickups and hauling related to gardening and landscaping? Sometimes the listing agent will drop any charges beyond the basic refuse pickup and forget to put the extras elsewhere even though the books reflect these charges.

A pet peeve of mine (and I have many) is when the listing agent simply lumps all utility expenses into one “utilities” line item. How can you double-check each separate utility expense item? Request separate itemizations. You get extra points for double-checking with each utility provider.

Remember to check for a sewer expense since this may be included on the tax bill rather than as a separate utility billing. When this charge is on the tax bill the listing agent may have “forgotten” to include it and just put 1% as the new tax figure. Voilà; no more sewer charge !

Watch out for a dropped month in a 12-month analysis. The last charge may have been paid late. This becomes even more significant if the charge is paid every other month.

Also, watch out if the overall percentage of total utilities / GOI exceeds around 6%. This may indicate overcrowding, master-metering or a water leak.

Accounting and Legal

This line item is often omitted and I see why. The owners total accounting bill includes work for the subject property, but the bill is not separated out for the property. I usually assign some nominal number to this work as an estimate. Look for legal expenses in the books as lots of entries may indicate systemic, negative tenancy issues like sloppy tenant screening.

Licenses / Permits

The City of Santa Barbara has an annual business license requirement for every apartment building based on income and yet this charge is seldom reflected in the listing agent’s expense statement. It could be a nefarious omission or just ignorance. Frankly, I vote for the latter. It will usually be reflected on the owner’s books as their interests are in maximizing expenses whereas the listing agent’s interests are in minimizing expenses. View the application that includes how to calculate the amount in the city of Santa Barbara here – https://goo.gl/dpKjex

Advertising

The management company may bill this out separately or it may be buried in singage installation, promotion or somewhere else. If I don’t see it, I put in a nominal expense.

Supplies

Most management companies will break out this separate line item from maintenance. I drop it and incorporate it into the price-per-unit maintenance estimate that I use.

Contract Services

This would be for say landscaping, gardening, cable TV, Dish TV, internet, pest control, fire extinguisher maintenance, furnishings in furnished units and anything that is an ongoing, contracted expense.

I usually see gardening grouped with landscaping. Some landscaping should be reflected in reserves because it may be a capital expense. Be sure that these line items reflect any extra hauling expenses or that these additional costs are reflected in the refuse line item or elsewhere.

Reserves

This would be reserves for capital expense items, i.e. roofing, asphalt replacement, appliance replacement and basically any item that your accountant would tell you needs to be capitalized rather than expensed.

Now for some esoterica! Where should the reserves line item go? Sometimes it appears in expenses. Sometimes it appears below the expense total as a separate itemization. Rather often it is entirely missing! The CCIM form places it below expenses and NOI. Appraisers have waffled back and forth on where to place this line item with the current norm appearing to be to include it in expenses.

To obtain an accurate cost estimate for reserves, an appraiser must itemize each possible capital item, estimate the lifespan of each item, estimate the remaining useful life of each item and then provide for an annual sum that should be set aside for its eventual replacement. Of course, this will vary property to property. There are tables and guidelines for this, but wow that is a lot of work! Some appraisers will do this. I’ve never seen an agent do this though. I don’t do it. Sometimes it’s estimated as a price per unit (my choice).

Why is the placement of the reserves line-item important? It is usually a large number, often near to or exceeding the maintenance figure. So, if it is not included in expenses, the cap. rate estimation (NOI/Price or Value) will be higher. Learn what the norm is in your area so that you are comparing apples to apples. Remember, an apple a day…oh! I said I wouldn’t do that cliché thing again. If the norm is for reserves to be included in expenses and the listing agent has put it below the NOI line, the cap. rate looks better, but it is misleading when trying to determine if the deal is good compared to other opportunities or past sales.

Wrap-up

The real-world overall expense ratio on a typical, separately-metered local apartment building is going to be around a third to 40% of GOI. Sorry, but that’s reality. If you see any substantial variation from this general rule look out! Something is askew or entirely unique.

Master-metered and high-abuse properties feature higher expense percentages. A brand-new or entirely remodeled building will feature lower expenses.

So, there you have it! I hope that you are now more aware of how these line items can be, shall we say, “nudged”. Remember, the APOD in the marketing flyer represents the property in its best possible light. What you want are just the true facts.

____________________________________________________________________________________

[1] GRM (Gross Rent Multiplier) – Sales price or value / annual scheduled GOI (Gross Operating Income) – The lower the better

[2] Cap. rate (capitalization rate) – NOI (Net Operating Income) / sales price or value – the yield of the property without respect to debt – The higher the better

[3] Santa Barbara County – South Coast Apartment Market Survey, Dyer Sheehan Group, Inc. (805) 653-8100, www.dyersheehan.com

[4] GOI Gross Operating Income – Gross income after vacancy and credit losses plus other income

[5] CCIM APOD forms https://goo.gl/n5xcW8

[6] Apartment Building Appraisers & Analysts, Inc. Joseph G. Queen 562-434-0571 jgqueen@aol.com

____________________________________________________________________________________

Brian Bailey is the broker-owner of Central Coast Investments. He is one of the leading multifamily brokers on the Central Coast covering Santa Barbara, Ventura and San Luis Obispo counties. He has a four-decade history of success and has been a member of the SBRPA since 1983.

I decided that I’d attend the South County event as this is the base of most of my business. Note that the UCSB Economic Forecast Project also provided attendees a 138-page study of South Santa Barbara County with lots of helpful material geared towards our local geographic area.

I decided that I’d attend the South County event as this is the base of most of my business. Note that the UCSB Economic Forecast Project also provided attendees a 138-page study of South Santa Barbara County with lots of helpful material geared towards our local geographic area.

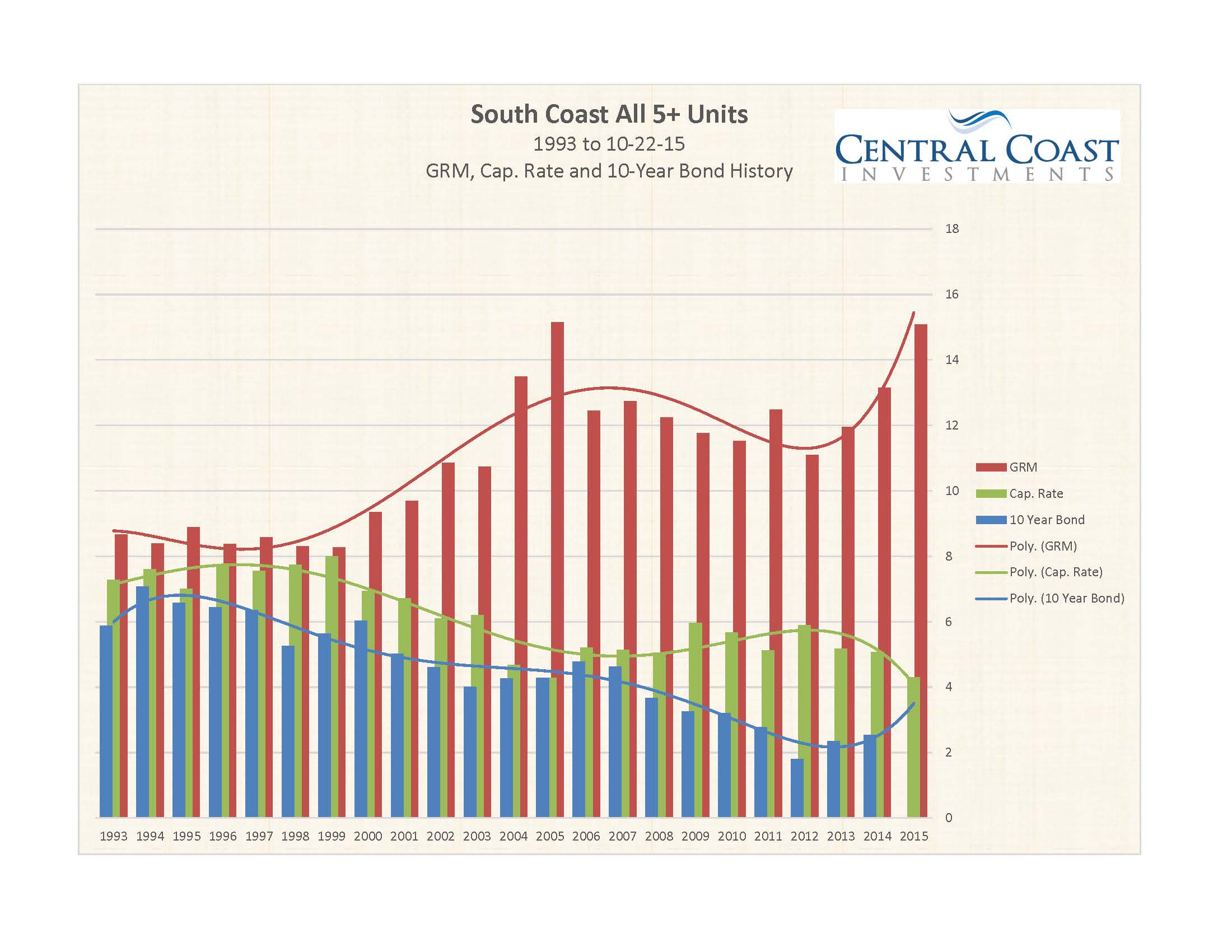

Click chart to enlarge.

Click chart to enlarge.